Pension Risk Transfer

Your plan. Our priority. That’s Quantum

As the focus of many organisations shifts towards Defined Contribution (DC) offerings, managing legacy Defined Benefit (DB) plans can become a significant drain on resources and a source of financial uncertainty. Fluctuating interest rates, longevity risk and administrative burdens can impact your balance sheet and distract from your core business activity. A pension risk transfer transaction can benefit organisations looking to de-risk and re-direct resources, whilst still delivering legacy obligations to members.

Partners in Confidence: Securing your future. Simplifying your present.

At Quantum Advisory, we have a deep understanding of the pressures faced by small and medium-sized schemes. We provide a big name service on a first name basis, acting as your partners in confidence to navigate the complexities of pension risk transfers to deliver the best possible outcomes for your scheme and members.

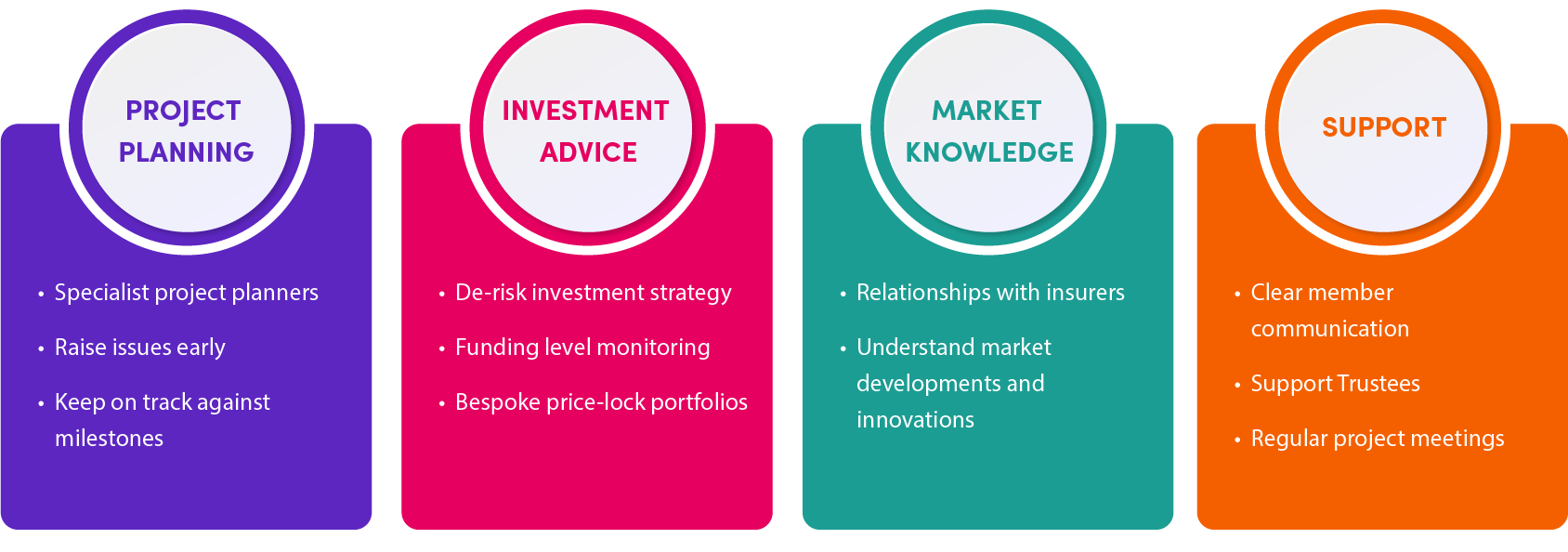

Our dedicated team of risk transfer experts, comprising senior actuarial and investment consultants, data specialists, project managers and DC experts, bring extensive experience to every project. The team have relationships with and are in regular contact with all the key insurance companies and pension consolidators and so understand their appetite and capacity, meaning clients can focus their time and resources on providers able to deliver transactionable solutions in the timeframes required. We take the time to truly understand your business and your scheme’s specific needs, ensuring a tailored approach that aligns with your goals. And we believe in simplifying the complex, using clear and straightforward language to explain the options and guide you through every step of the journey.

With Quantum you get good people, providing high-quality, reliable and pragmatic risk transfer advice and services, at a price you can believe in. Allowing you to focus on your future with confidence, secure your employees’ benefits, and simplify your present.

We have a packaged service ready to manage the risk transfer journey.

Find out more about Amanda Burdge here

For any pension scheme considering a buy-in or buy-out transaction, preparation is key. There are several areas that trustees should be reviewing now to help any risk transfer project run smoothly and also to achieve the best pricing from the market including:

- Ensuring scheme documentation is in good order

- Preparation of a full, legally reviewed benefit specification

- Reviewing membership data and collecting any missing data items

- Feasibility analysis.

Not only will these steps save time and reduce costs, they are also vitally important to enable schemes to demonstrate to the insurance market that they are serious about transacting when seeking quotations.

We actively monitor pricing across the market and provide regular updates on both insurer trends and pricing. Together with our advanced funding level monitoring for schemes, this work helps us identify pricing opportunities in the market and enables us to secure a quick transaction at the optimum price when these opportunities present themselves.

The risk transfer marketplace is constantly evolving, and the potential use of consolidation vehicles is one for consideration by trustees. Our knowledge of the market and early engagement with providers can help us demystify the options for schemes and advise trustees on all options.

We work with clients of all sizes to proactively manage their scheme liabilities in preparation for a risk transfer exercise. This includes undertaking pension increase exchange (PIE) and enhanced transfer value (ETV) exercises, which can deliver material reductions to scheme liabilities and by association funding obligations. We also assist with consolidating and simplifying complex benefit structures to make them easier for insurers to price attractively or administer.

Importantly, we consider your scheme’s long-term end-game to ensure any liability management or consolidation exercise undertaken do not negatively impact any future buy-in pricing.

We provide expert advice on investment strategy at all phases of the risk transfer journey. Our goal is to align scheme assets with insurer pricing and minimise funding level volatility. This ensures you can effectively plan for a risk transfer exercise, achieve your funding target, and avoid falling short of the buy-in price. We work closely with insurers to manage price-locks between quotation and completion.

What is a pension risk transfer?

Pension risk transfer is the process of removing pension liabilities from a scheme's balance sheet by transferring them to an insurer, through a bulk annuity purchase, or pension consolidation vehicle.

How does pension risk transfer work?

Trustees pay a premium to transfer all or part of their obligations to an insurance company or consolidator, who then assumes responsibility for paying member benefits. The pension risk transfer market offers several types of pension risk transfer including buy-ins, buy-outs, and longevity insurance. This eliminates volatility from interest rates and longevity risk while securing member benefits. At Quantum Advisory, our dedicated risk transfer team of senior actuarial and investment consultants, data specialists and project managers brings extensive experience to every project, with relationships across all key pension risk transfer companies and pension consolidators to help identify solutions and meet your required timeframes.

What's the difference between buy-in and buy-out?

A buy-in involves purchasing a bulk annuity policy that matches scheme liabilities - the scheme remains in place with the policy held as an investment. A buy-out transfers all liabilities directly to the insurer who pays members - the scheme then proceeds to wind up.

Buy-ins offer an intermediate step to lock in pricing, often preceding full buy-out. Buy-outs provide complete exit, eliminating all ongoing obligations. Both require careful preparation including documentation review, completing GMP equalisation, and data cleansing. Quantum Advisory actively monitors pension risk transfer pricing across the market and provides regular updates on insurer trends. Together with our advanced funding level monitoring, this helps us identify pricing opportunities and the ability to secure quick transactions at optimum prices when they arise.

What are pension consolidators and how do they differ from traditional insurers?

Pension consolidators, also known as pension superfunds, are alternative pension risk transfer providers offering another endgame option for DB schemes. Unlike traditional bulk annuity providers who are highly regulated insurers, pension consolidators operate under different regulatory frameworks, typically accepting schemes at earlier funding stages and potentially lower cost, though without the same regulatory capital protections. They can provide a stepping stone in the pension risk transfer journey for schemes not yet ready for traditional buy-in or buy-out. The pension risk transfer market continues evolving with new consolidator vehicles emerging. At Quantum Advisory, our knowledge of the market and early engagement with pension consolidators and pension risk transfer companies helps us demystify the options for schemes and advise trustees on all available routes, considering your scheme's long-term endgame.

What liability management exercises can prepare schemes for risk transfer?

Liability management exercises reduce and simplify scheme obligations before pension risk transfer transactions, improving pension risk transfer pricing. Enhanced transfer value exercises offer members cash incentives to transfer out, reducing liability while providing member flexibility. Pension increase exchange exercises allow members to swap inflation-linked increases for higher fixed pensions, simplifying benefits for bulk annuity providers. Combined with completing GMP equalisation and consolidating complex benefit structures, these can deliver material reductions to liabilities. Quantum Advisory works with clients of all sizes to proactively manage scheme liabilities in preparation for risk transfer, including undertaking pension increase exchange and enhanced transfer value exercises. Importantly, we consider your scheme's long-term endgame to ensure any liability management exercises undertaken don't negatively impact future buy-in pricing.

What is pension de-risking and how does it relate to risk transfer?

Pension de-risking involves reducing financial risks associated with DB schemes through investment strategies and liability management. Investment de-risking means aligning scheme assets with insurer pricing to minimise funding level volatility, ensuring schemes can plan effectively for pension risk transfer exercises. This involves hedging interest rate and inflation risks and shifting to lower-risk assets. De-risking also includes liability management exercises to reduce obligations. The ultimate step is pension risk transfer itself - buy-in or buy-out - completely removing risks from the sponsor's balance sheet. Quantum Advisory provides expert advice on investment strategy at all phases of the risk transfer journey, aligning scheme assets with insurer pricing and minimising funding level volatility. We work closely with bulk annuity providers to manage price-locks between quotation and completion, ensuring you can achieve your funding target and avoid falling short.

What happens during pension scheme wind up after a buy-out?

Pension scheme wind up is the final phase following buy-out, where the scheme is formally closed and all administrative obligations completed. After the insurer assumes responsibility for member benefits, trustees must distribute remaining assets, settle expenses, obtain clearances from HMRC and the Pensions Regulator, and complete final documentation including ensuring GMP equalisation is finished. Any surplus assets are typically returned to the sponsor. While buy-out transfers payment obligations, pension scheme wind up ensures full legal closure, typically taking several months and marking the successful conclusion of the pension risk transfer journey. Quantum Advisory manages the entire risk transfer journey from initial preparation through to final wind-up, ensuring proper documentation is in place, benefit specifications are legally reviewed, and all necessary data is collected. Our dedicated project managers ensure wind-up is completed to agreed timelines and budgets.

Simon Hubbard, Principal Consultant at Quantum Advisory looks at the various endgame options available to trustees of a mature pension scheme.

Find out more about Simon Hubbard here

Robin Dargie, Senior Consultant at Quantum Advisory looks at the financial strength of mastertrusts and insurers focussing on what trustees should initially consider for DC and DB schemes.

Find out more about Robin Dargie here

Stefano Carnevale, Senior Investment Consultant looks at price lock portofolios and explores different ways clients can design and tweak their investment strategies to better align assets with movements of insurance premiums.

Find out more about Stefano Carnevale here

Matthew Elguezabal, Data Services Manager discusses the role of data preparation and management in buy-in and buy-out projects and why it is an often overlooked part in a de-risking strategy.

Find out more about Matthew Elguezabal here

Case studies

Further reading

Journey Planner Q1 2025

Journey Planner Q3 2024

Journey Planner Q2 2024

Talk to our team

Get in touch with our friendly team today to talk about how we can help your business.