SA Brain

Quantum has been advising the Trustees of this Defined Benefit pension scheme (‘the Scheme’) on investments for several years. The Scheme has assets of circa £65 million, and regularly reviews it’s investment strategy to reflect changes in the Scheme’s funding position, the Employer’s covenant, as well as developments in markets and investment funds.

When Quantum were appointed, the Scheme had a simple investment strategy that invested in traditional asset classes (public equities, corporate bonds, government bonds and cash). We worked with the Trustees and the Employer to understand their investment beliefs and risk tolerance. This resulted in the inclusion of new asset classes, including structured equity, private markets, diversified growth funds, strategic bonds, Liability Driven Investment (“LDI”), funds of hedge funds, and cashflow driven Investment (“CDI”). Therefore, the Scheme’s investment strategy has been made more efficient, funding risk has been reduced and outflows to meet benefit payments have been better matched.

Furthermore, we designed mechanisms that enable the Trustees to track the Scheme’s funding level, relative to the targeted flightpath. This enables the Trustees to reduce risk when/if the Scheme’s funding level experience is better than expected. This has involved implementing daily funding level tracking, and an automated framework to switch from growth assets to matching assets to “bank” any positive funding level experience. A qualitative overlay is also applied to ensure the Scheme’s investment strategy remains fit for purpose.

As the Scheme was getting closer to being fully funded on a Technical Provisions basis, we worked with the Trustees to adopt a secondary funding objective of moving the Scheme towards self-sufficiency.

The Company’s covenant was strong, until more recently, when Covid-19 placed severe stress upon revenues. Considering this development, we helped the Trustees to introduce the following risk reduction/protective measures to stabilise the Scheme’s funding level:

- Increasing the level of interest rate and inflation protection: This was done on two occasions to insulate the Scheme’s funding level from adverse movements in interest rates and inflation, reflecting the perceived weakening of the Company’s covenant. The increase was initially to 75% of assets and then to 100%. These asset allocation changes have served the Scheme particularly well as real and nominal gilt yields have fallen further since implementation.

- Replacing the Scheme’s equity holdings with a structured equity product: Structured equity is designed to provide growth with protection by contractually defining the range of outcomes that can be achieved. It provides downside protection on the assets when equities fall and is funded by capping the level of positive return the Scheme can achieve. The return cap has been set to provide sufficient upside to support the equity return assumptions that factor into the actuarial discount rate and provides downside protection when equity markets fall. We advised the Trustees on the appropriate level of return and degree of downside protection to target.

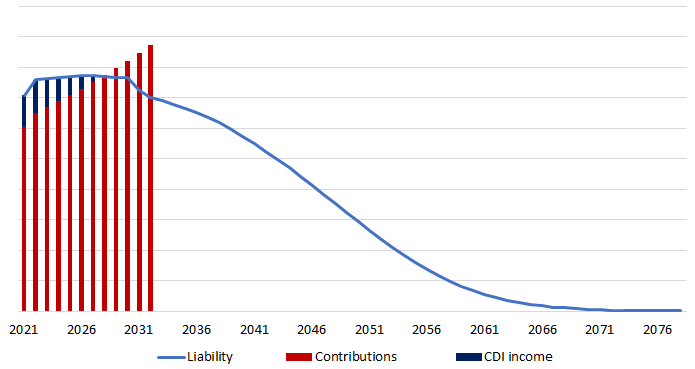

- Introducing a CDI strategy: This involves investment in a portfolio of high-quality corporate bonds (which are income generative), and a cash holding. Cash (from the corporate bonds) is paid to the Scheme on a quarterly basis and is comprised of coupon payments and return of capital (on the underlying bonds when they mature). This cash, together with Company contributions, is used to meet the Scheme’s cashflow requirements. This provides certainty that benefit payments can be met as they fall due, whilst at the same time avoiding the sale of Scheme assets during periods when prices are depressed. The strategy was put in place to cover cash flow until 2025 and will be reviewed in line with the next actuarial valuation, when it will be “topped up” to ensure future cashflow remains “matched”. The following graphic illustrates this.

The Trustees have resolved the uncertainty around the Company’s covenant and are now considering the long-term investment strategy for the Scheme. Whilst a low-risk strategy will be adopted, we are looking at how the level of required return can be generated in the most efficient way.